3 min read

Retiring early requires disciplined saving and careful planning under the best macroeconomic and market scenarios. When you’re retiring into an inflationary environment, there’s an added layer of complexity. But after the challenges of last year, that’s exactly what many people are doing. The realization that time is finite, and there are better ways to spend it than working has an unprecedented number of people age 54 and under self-identifying as “pre-retirees,” meaning they will retire within the next five years.1

Retirement Planning 101

It’s all about the budget – no matter how you define that. When it comes to retirement income, the starting point is what you spend now. The rule of thumb used to be that retirement would likely be less expensive than your working life, so you wouldn’t need to replace as much income. But especially when you’re retiring early, it’s important to be realistic about what you’ll be spending. In the first decade or more of retirement, it’s possible that with travel and other adventures, you’ll spend more than you did when you were working. Expenses don’t generally tend to dip until the mid-late part of retirement, and then they rise again largely due to healthcare costs at the end of retirement.

Creating an income stream that meets your needs across your retirement requires skillful planning. Particularly if you already have a portfolio constraint, such as a concentrated stock position, an asset allocation that hedges risk, allows for growth, and generates income will be the key feature of your plan. But inflation affects different asset classes in different ways – and even how much inflation there is can create the need to pivot and rebalance.

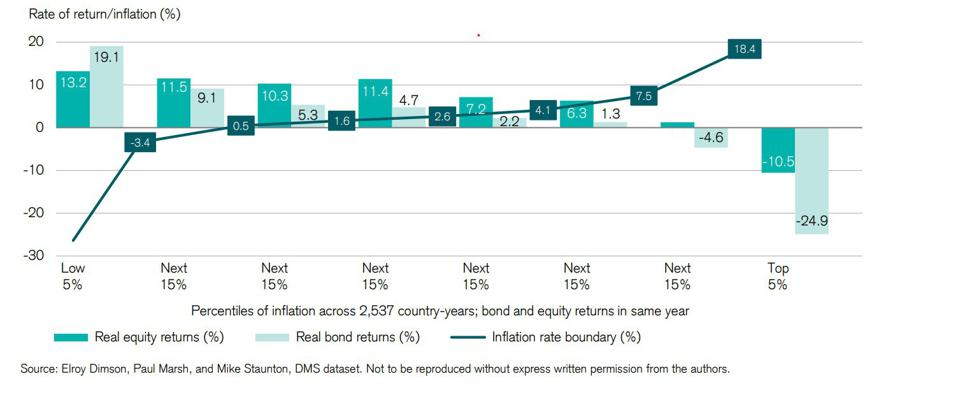

Stocks, Bonds, and Inflation

The chart below details how stocks and bonds respond to different levels of inflation. While very high inflation is bad for both asset classes (and everything else), inflation levels slightly below the Fed’s target average of 2% are positive for equities. However, that changes quickly. According to the chart below, if the current level of inflation – projected at 3.4% for this year – were to persist or increase, we could expect to see equity returns drop significantly.

Bond returns, of course, don’t do well at all in inflationary scenarios. Inflation pushes up interest rates, which pushes down bond prices (bond prices and yields have an inverse relationship). Given the low levels that bonds yields are already at, pushing yields up won’t gain much of an advantage over inflation to provide income; it would just result in sacrificing price return.

But the Equity Markets are Notching New Highs

Yes, they are. And home values have gone through the roof. Both of which are making deciding to retire earlier even more irresistible. But while home prices tend to outpace inflation – that only works while you own your home. If you sell it, invest the proceeds, and decide to tour the country in an Airstream, you’re right back where you started: at the mercy of inflation. And while the markets are notching new gains, we also see increased volatility. Beyond the headline-driven volatility due to the continued choppy recovery from the pandemic, unexpected inflation can also cause market volatility. Markets are forward-looking – today’s prices factor in future expectations. When inflation jumps more than expected, it tends to be very negative for stocks.

The other impact of inflation has been on what stocks are notching gains – and so far this year, value is outpacing growth. According to ETF Trends data, Value ETFs saw $53 billion in net inflows in the first half of the year, while growth funds lost $331 million. Growth stocks struggle in inflationary periods because most of their earnings are in the future – and inflation makes them worth less. When this trade ends is anyone’s guess. It is still a trade, though, and not a paradigm shift at this point. This makes it a little more difficult to plan a portfolio allocation that can withstand shocks, produce consistent income, and still grow.

The Bottom Line

Retiring early is achievable – even with a volatile market and increased inflation concerns. It just requires a little more thought and planning and an obvious idea of all the other pieces so the puzzle – so that there aren’t any surprises down the road. An investment plan that makes careful use of risk, is planned around all your assets, and is flexible enough to cover both market and personal ups and downs is still the gold standard for navigating a successful retirement.

- March, 2021 survey results of 60,000 households from market research company Hearts and Wallets.

We Deliver Content Like This Every Month to Your Inbox. Sign Up to Start Receiving Updates

Related Posts

Retiring Early and Bridging the Gap to Medicare

Early retirement may be planned or unplanned, but either way, stopping work results in big...

Tax Increases Aren’t Just About Rates

The Build Back Better Act has gotten a lot of press for the intended means to pay for it – by...

Investing in Retirement: It’s About Avoiding Volatility

You’ve been saving and investing diligently and now retirement is finally here. You may be at the...