4 min read

.png)

Timing is one of the biggest decisions you need to make in planning for retirement. There are of course lifestyle impacts you will need to sort through, but deciding when to take social security and determining distributions from your retirement plan can have long-term financial implications.

The good news is that successfully navigating the timing with some creativity can set you up to begin your retirement in great shape. We outline a strategy that may allow you to maximize social security benefits while minimizing required mandatory distributions.

Key concepts we’ll cover: Calculating social security benefits for early, full and late retirement, factoring in your life expectancy, required mandatory distributions (RMDs) from retirement plans.

Social Security – When to Start

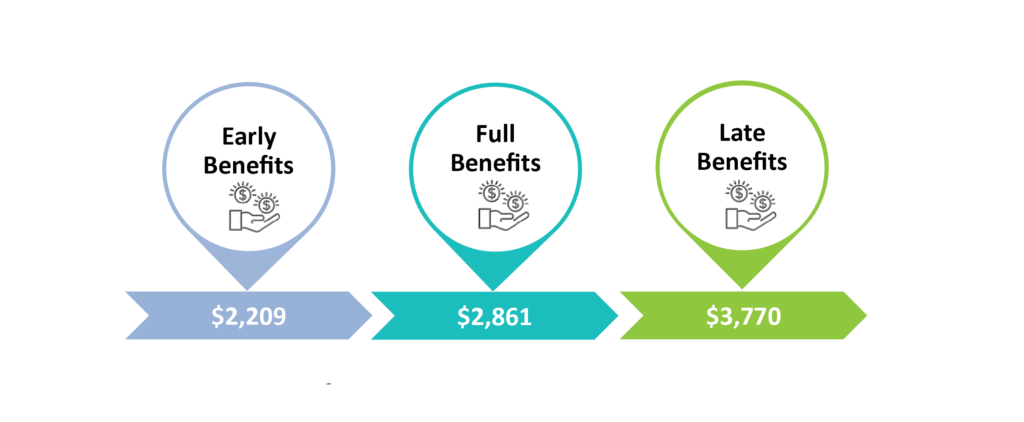

In 2019, “full retirement age” at which you are entitled to full benefits is 66* years old. You can retire as early as 62, but this is considered “early”, and your benefits will be reduced from the full benefit amount by as much as 25% per year. The Social Security Administration (SSA) calls these early benefits. If you delay retirement until after age 67, you are entitled to what the SSA calls late benefits, which are an increase over full benefits by 8% for every year you delay, up to age 70. The decrease or increase is permanent – that sets the baseline number you will receive for the rest of your life.

The table below reflects the actual maximum monthly benefit possible in 2019 and the adjustments for early and late retirements. As can be seen from the numbers, early benefits are less than full benefits and late benefits are more than full benefits. Essentially, there is a penalty for retiring early (before age 67) and a reward for retiring late (after age 67).

*Source: AARP For birth years 1943-1954, retirement age is 66; it will gradually rise to 67 for those born in 1960 or later.

Knowing Your Estimated Benefits

To find your estimated benefits based on your employment history, go to the SSA Retirement Benefits Estimator. You’ll need to create an account and verify your identity to access your full employment history and your estimated benefits. The Benefits Calculator lets you choose any retirement date and gives you the percentage your benefits will increase or decrease. You can multiply that percentage by your estimated benefits to find out the impact.

Is the Breakeven Important?

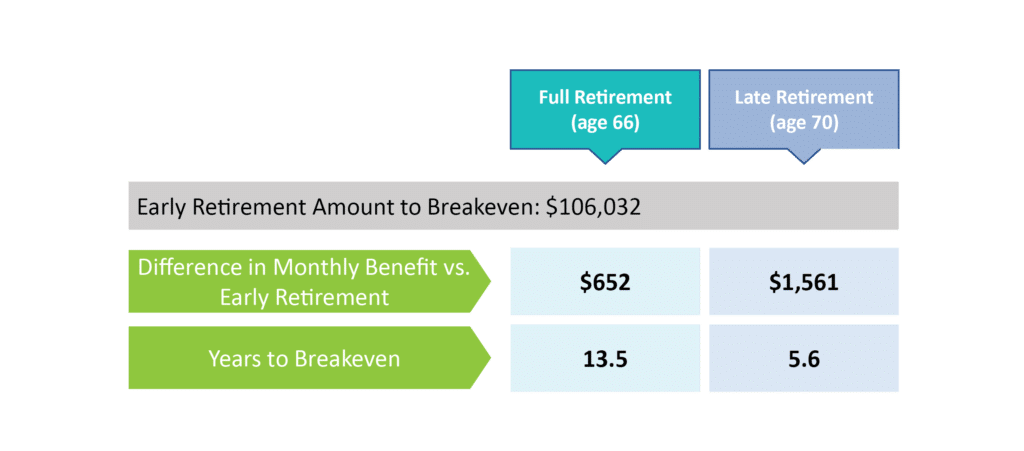

Delaying retirement results in larger monthly payments, but you’ll receive fewer of them. That’s why some people focus on the “breakeven” analysis in making the decision. The breakeven is the point at which the total of the difference between full or late benefits and early benefits equals the total amount the early retiree received while the full or late retiree was receiving nothing. In other words, the choice is between retiring early and getting less per month or retiring later and getting more. Depending on how long the retirement lasts, the larger monthly payments may result in more total benefits – but the months or years in which the early retiree is receiving benefits while the late retiree isn’t needs to be taken into account.

Using the maximum benefit amounts for 2019 detailed above, the early retiree receives $106,032 in the four years before full retirement at age 66. The chart below details the difference in the amount of the monthly benefit for full and late retirement vs. early retirement. The number of years to breakeven – meaning the age at which the greater monthly benefit for full and late retirement adds up to more than $106,032 – is age 79 for full retirement and age 75 for late retirement. After those ages, the later retirees receive more money over their lifetime than the early retiree.

Factoring in Life Expectancy

In addition to understanding your benefits options and breakeven points, life expectancy should be a factor. In 2019, life expectancy for a man born in 1960 was 83 years, according to the Social Security Administration. Current health and family longevity history of course make a difference, but for most people, from a financial standpoint it’s worth it to delay retirement.

A Lifestyle-Based Approach

Lifestyle factors play into your social security decisions as much, if not more, than life expectancy and estimations. For instance, you may decide to delay because you aren’t ready to stop working, or you need a few more years of full salary to save for retirement, or you may want to keep your company health care plan longer. For some people, retiring as early as possible and spending time catching up with family, committing to an avocation or new business, or fulfilling travel goals while relatively young is important.

Bottom Line

When to start on your retirement journey is a personal decision with many moving parts – and it requires thoughtful, careful analysis. Working together, your financial advisor and you can map out a plan that incorporates your lifestyle and your goals and makes sound financial sense.

We Deliver Content Like This Every Month to Your Inbox. Sign Up to Start Receiving Updates

Related Posts

Five Money Moves to Make in 2022

Working out more, prioritizing self-care, and spending less time on your devices are all great...

Over 50? Here's How to Boost your Savings

How much do you need for retirement? Well, investment research firm Morningstar has a handy but...

Traditional Financial Planning – With A Non-Traditional Edge

Traditional Financial Planning – With A Non-Traditional Edge

For decades, DeWitt Capital has always...